In a Kansas divorce, everything you own lands on the table the day someone files. This guide gives you the math to get it back.

Most states let each spouse keep "their half." Kansas doesn't work that way. Under the state's "all-property" rule, the instant a divorce petition is filed, every asset either spouse owns — the 401(k) you started years before the wedding, the house you bought single, the inheritance from your grandmother, even the appreciation on a brokerage account in your name only — is swept into one shared pool and divided in whatever way a judge decides is "just and reasonable." Not automatically 50/50. Just and reasonable.

That single rule is why so many Kansans go to bed terrified they'll lose a legacy they thought was safe. And here's the part nobody tells you: your separate property is only protected if you can prove its value on your wedding day — with documents, not testimony. Guess wrong, mix an inheritance into a joint account, or add a spouse's name to a deed, and the claim can vanish entirely.

The problem isn't finding the forms. It's knowing the numbers to put in them.

The State of Kansas hands you every official divorce form for free at the Kansas Judicial Council (kjc.ks.gov) — and you should download them there. But the court clerk is legally forbidden from telling you how to fill them out. They can't tell you how to value your house. They can't calculate your spousal maintenance. They can't trace your premarital 401(k) or tell you whether a Type A, B, or C order splits your KPERS pension.

So you're left with two options that both cost you:

- Download the free blank forms — and stare at empty boxes with zero guidance on how to negotiate or calculate a single number.

- Hire an attorney — at $150–$350 an hour on top of a $1,500–$5,000 retainer, where the most expensive hours are the ones spent organizing documents you could have organized yourself.

There's nothing in between. Until now.

The Kansas Numbers-First Method

This guide is built on one idea: the state gives you the empty boxes for free — we give you the math, the formulas, and the Kansas-specific strategy to fill those boxes out correctly before you sign anything or walk into a lawyer's office.

It is not a stack of forms (those are free). It is not generic financial advice. It is a process-navigation and financial-modeling toolkit built specifically around Kansas statutes — the all-property rule of K.S.A. § 23-2801, the ten equitable-distribution factors, the Johnson County maintenance formula, the KPERS coverture fraction — so that every number you bring to the table is defensible, organized, and working for you instead of against you.

For — less than an hour of an attorney's time — you get the exact worksheets and calculations that make the difference between a fair settlement and one you regret for a decade.

What's inside — and the fear each part solves

- The Separate-Property Tracing Worksheet — one row per asset, building the documented, wedding-day-to-today paper trail Kansas courts require to restore your "entry value." Solves: losing an inheritance or premarital home to the all-property sweep because you couldn't prove what it was worth going in.

- The Ten-Factor Scorecard — score yourself on each of the ten statutory factors a judge actually weighs under K.S.A. § 23-2802(c), so you can argue for a "just and reasonable" split instead of hoping for one. Solves: walking in with no idea whether your case leans 50/50 or something else entirely.

- The House Buyout Calculator — the exact Kansas formula (Appraised Value − Mortgage) × Equitable Share, plus five structural options for the home and a refinance-deadline checklist. Solves: overpaying for a buyout, or losing the house — and your credit — because the refinance wasn't nailed down.

- The Retirement Offset Matrix & QDRO checklist — model trading the 401(k) for home equity on an after-tax basis, plus the KPERS/KP&F pension rules (Type A/B/C orders, coverture fraction, the pre-approval contact). Solves: accepting a "50/50" retirement split that's really lopsided once taxes and pension rules are counted.

- The Johnson County Maintenance Modeler — run the tiered 25%/22% amount formula and the duration/121-month-cap timeline with a worked example. Solves: not knowing whether you'll pay (or receive) $400 or $1,400 a month, or for how long.

- The Debt-Allocation Ledger & refinance-trap checklist — split credit cards, student loans, and joint IRS liability, with the warning most people learn too late: a decree doesn't bind your creditors. Solves: getting chased for your ex's debt years after the divorce is "final."

- The After-Tax Negotiation Ledger — value every asset by FMV, cost basis, and after-tax worth, because equal on paper is rarely equal after the IRS takes its cut (Section 1041, capital gains, the home-sale exclusion). Solves: splitting the estate "evenly" and quietly getting the worse half.

- The Domestic Relations Affidavit (DRA) prep worksheet — gather every number the mandatory, notarized Rule 139 disclosure demands, mapped to its four sections, so a clerk doesn't reject your filing and a mistake doesn't unravel your settlement years later. Solves: a rejected filing or a perjury exposure from a sworn form filled out wrong.

Who this is for

- You earn too much to qualify for free legal aid but can't justify draining thousands from the marital estate on billable hours.

- You're representing yourself and need a sequential map from "everything's on the table" to a signed decree.

- You are hiring a lawyer — and want to walk in with your assets valued, your maintenance modeled, and your tracing done, so you're paying for advocacy, not data entry.

- You have something to protect: a premarital home, an inheritance, a pension, a business, or a retirement account you built.

Why not just use the free tools?

Because they stop exactly where the hard part starts.

- The Kansas Judicial Council (free) gives you legally accepted blank forms — and staff who are barred by law from explaining a single strategic consequence of how you fill them in.

- Kansas Legal Services (free) is excellent for simple, low-income cases, but strict income limits shut out the middle class, and its templates have no asset-buyout or QDRO math.

- 3 Step Divorce ($299) and Hello Divorce ($99–$499/month) automate filling out the forms. Neither helps you value a house, trace a premarital 401(k), or model a retirement offset before you commit the numbers.

- QDRO.com ($399) drafts one retirement order and nothing else — no house, no debt, no maintenance, no strategy.

- A private attorney ($1,500–$5,000 retainer) can do all of it — while the meter runs on hours you spend handing over documents you could have organized for .

This guide is the missing bridge: the math and worksheets that let you design a fair, structurally sound agreement first — then fill out the free forms, or hand a mediator or attorney a clean, organized file.

An honest promise

This is an educational financial-organization and process-navigation tool. It is not legal advice, it doesn't represent you in court, and it doesn't pretend a download replaces a lawyer when your case genuinely needs one — it tells you plainly when to bring one in. What it does promise: to hand you the exact Kansas-specific calculations and worksheets that most people pay hundreds of dollars an hour to have someone else assemble.

Try it. Work through the tracing worksheet and the maintenance modeler. If it doesn't give you more clarity and control over your financial split than anything else you've found, it isn't doing its job — reply to your receipt and we'll make it right.

Start where you are

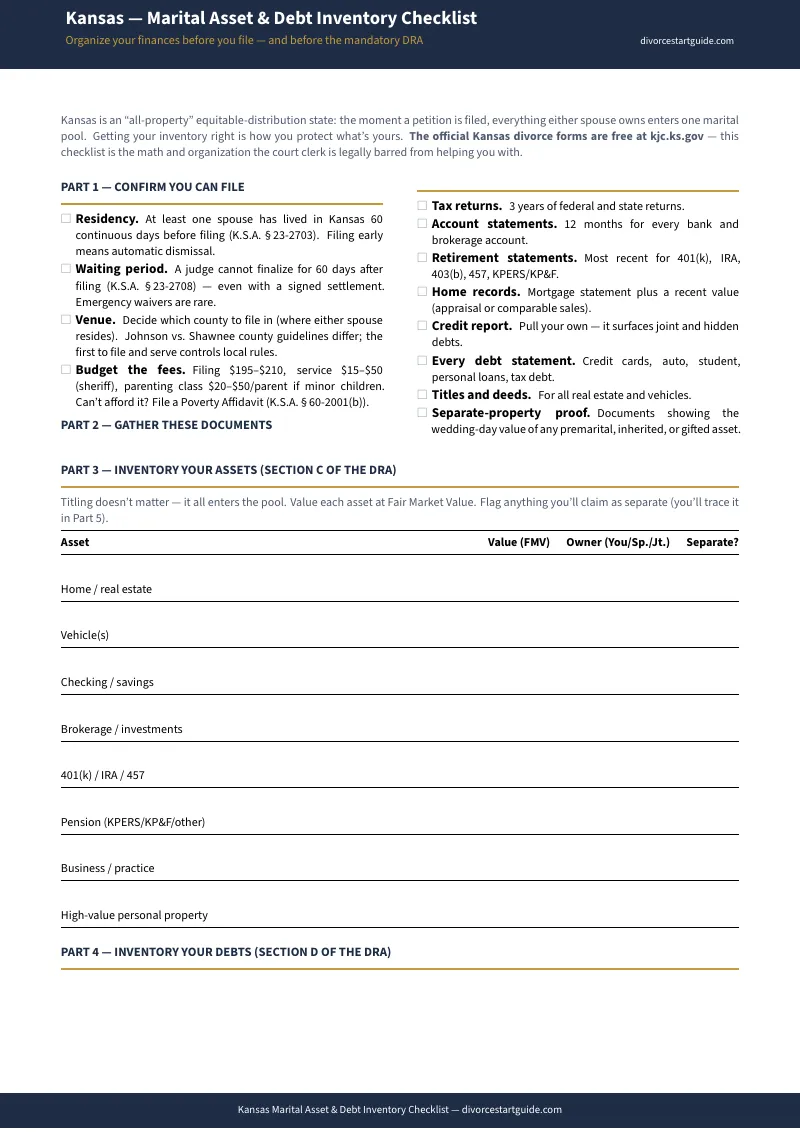

Not ready for the full guide? Begin free with the Kansas — Marital Asset & Debt Inventory Checklist: a one-page inventory that captures every asset, debt, and property item in one place — the raw numbers you'll need before you touch the state's mandatory Domestic Relations Affidavit.

When you're ready to turn that inventory into a settlement — with the tracing, the buyout math, the maintenance formula, and the after-tax ledger — get the complete Kansas Divorce Financial Split & Asset Division Guide and fill in every box with numbers you can defend.