A "Fair Split" on Paper Can Cost You Tens of Thousands. Here's How to Know Before You Sign.

Your mediator or attorney says "we'll split the 401(k) 50/50." Sounds fair. But a $250,000 pre-tax 401(k) and a $250,000 savings account are not the same asset — the 401(k) carries a future tax bill that can erase $60,000 or more of its real value. Your spouse's pension might be worth more than the house, but neither of you knows how to calculate it. And the settlement template your court provides contains a single generic line about retirement accounts — language that every plan administrator in the country will reject as incomplete.

Meanwhile, attorneys bill $300+ an hour, and most outsource retirement-specific work to a specialist anyway. QDRO drafting services charge $300–$700 per plan — but they only handle the final document, not the strategy that comes before it. Free court forms start and end your lawsuit. They don't calculate pension values, explain the tax treatment of rollovers, or walk you through the seven-step pipeline your plan administrator requires before releasing a single dollar.

The Division Readiness System

This workbook is the preparation and strategy layer that sits between your court's blank forms and your retirement plan's technical requirements. It doesn't draft court orders or replace your lawyer — it turns the most complex, highest-stakes part of your divorce into a concrete, sequential process you can actually follow.

Retirement accounts are governed primarily by federal law — ERISA, the Internal Revenue Code, DFAS regulations — regardless of which state or country you file in. The mechanics of splitting a 401(k) are identical in Texas and New York. IRA transfers follow the same IRC § 408(d)(6) rules everywhere. Military pensions use the same DFAS forms in every jurisdiction. This guide maps that universal administrative pipeline, then builds in explicit local-verification checkpoints that tell you exactly where your state's property rules, valuation dates, and division formulas take over — and how to confirm them.

What You Get

The Retirement Division Process Navigation & Strategy Workbook

A complete 12-chapter guide with fillable worksheets, administrator scripts, and jurisdiction-specific workflows — the full sequence from first inventory through final transfer execution. Your download includes the full guide plus 8 standalone printable worksheets you can bring to meetings, attach to settlement files, and hand to professionals:

- Retirement Account Inventory (standalone worksheet) — a fillable log for every 401(k), 403(b), pension, IRA, TSP, deferred compensation plan, and superannuation fund in the marriage, with a document request letter template and guidance on locating accounts a spouse hasn't disclosed

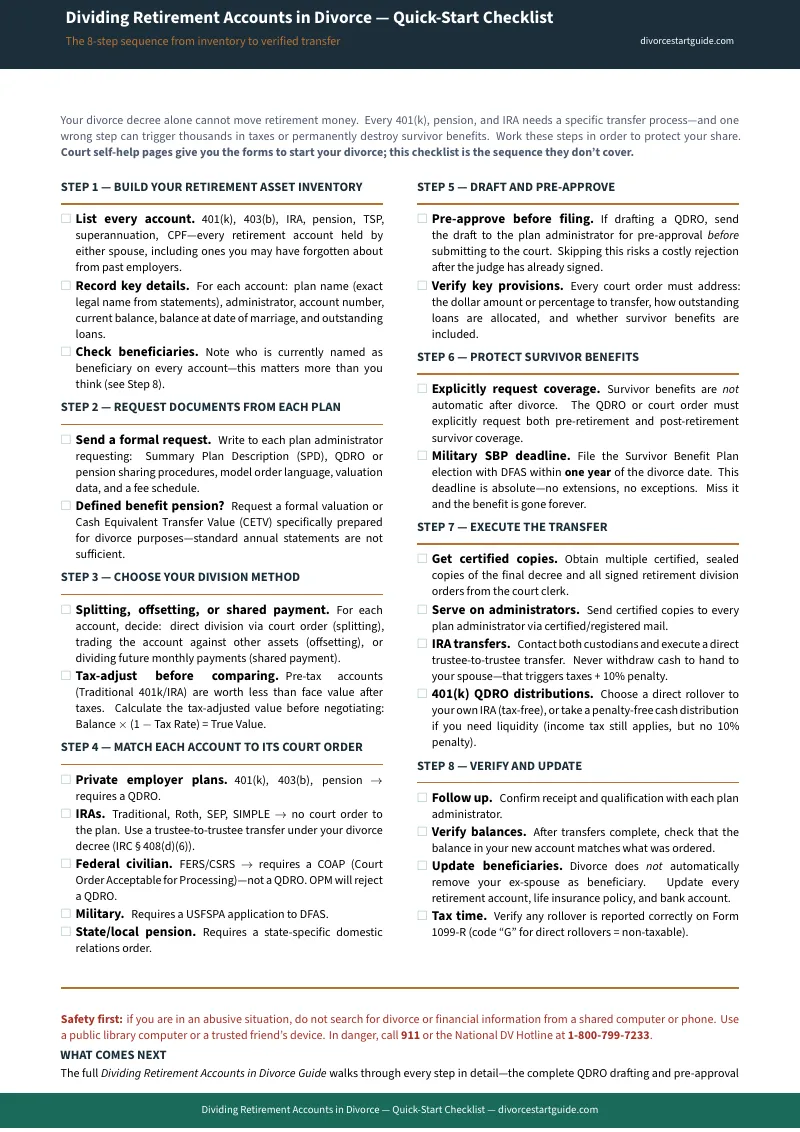

- QDRO Process Pipeline (standalone checklist) — a seven-step chronological checklist with date-tracking fields: request the Summary Plan Description, draft the proposed order, submit for administrator pre-approval, obtain the judge's signature, serve the certified copy, and confirm execution — with word-for-word scripts for calling HR departments

- Tax Trap Detector (standalone worksheet) — comparison worksheets that reveal hidden imbalances between pre-tax and post-tax assets, with the five most common tax traps and per-spouse calculation tables so you negotiate on real after-tax numbers

- Pension Valuation Workbook (standalone worksheet) — the coverture fraction calculator, valuation date selection table, and side-by-side comparison of splitting vs. offsetting vs. deferred distribution — with a per-account decision tracker

- Survivor Benefit Protection Checklist (standalone checklist) — pre-retirement and post-retirement survivor benefit action items, military SBP deadline tracking, and a benefit-by-benefit confirmation tracker

- Post-Divorce Execution Checklist (standalone checklist) — the 30-day, 90-day, and post-transfer action items that turn a signed decree into actual money in your account, plus a beneficiary audit tracker

- Division Method Decision Guide (standalone reference) — the four-question decision framework for choosing between splitting, offsetting, and shared payment, with a court-order-by-plan-type reference table

- Country Comparison Reference (standalone reference) — retirement division rules across 8 jurisdictions (US, UK, Canada, Australia, Ireland, South Africa, Singapore, Germany) — court orders, processing times, tax treatment, and first steps

- IRA Transfer & Rollover Decision Guide — step-by-step instructions for the trustee-to-trustee transfer, the critical difference between a direct transfer and cashing out, and the "QDRO cash-out exception" that lets an alternate payee take penalty-free distributions

- Government & Military Pension Division — separate workflows for federal civil service (COAP), military retirement (DFAS), state and local government plans, and the Thrift Savings Plan — with the specific forms, addresses, and jurisdiction requirements for each

Free Quick-Start Checklist — Retirement Account Division Readiness Check

A printable one-page checklist covering the first critical steps: which accounts need to be inventoried, what documents to gather from each plan, and the key questions to resolve before settlement negotiations begin. Yours free — a real head start on the most complex part of your divorce.

Who This Is For

- You're negotiating a settlement and want to understand the actual value of retirement assets — tax-adjusted, properly valued — before you agree to a division, not after the paperwork is filed

- You're representing yourself and need the step-by-step administrative sequence that court self-help desks and generic settlement templates don't provide — particularly the QDRO pipeline and IRA transfer rules

- You're preparing for mediation and want to arrive with organized statements, calculated values, and a clear picture of trade-offs so mediator hours go toward decisions, not data entry

- You have an attorney but want an independent checklist to verify nothing is being overlooked — plan-specific rules, survivor benefits, tax treatment, and the administrative steps between the judge's signature and the actual transfer of funds

- You're post-decree and your QDRO was rejected by the plan administrator, your ex-spouse is delaying, or you need to understand the rollover options before making an irreversible distribution election

Why Free Forms and Hourly Billing Don't Solve This

Court self-help centers hand out blank settlement templates that handle retirement accounts with a single line: "divide the 401(k) 50/50." That language fails because it doesn't specify the valuation date, how gains and losses between separation and distribution are allocated, who pays processing fees, how outstanding plan loans are handled, or whether survivor benefits are preserved. Plan administrators will reject it, and you'll be back in court refiling.

The DIY filing platforms don't fill the gap either. LegalZoom's divorce packages start around $499; 3 Step Divorce charges roughly $299. They generate standardized petition forms — they contain no retirement-specific guidance, no QDRO pipeline, and no pension valuation worksheets. For the actual retirement division, they'll refer you to a specialist.

QDRO drafting services like QdroDesk ($299 per plan) and TOVA ($700 per plan) handle the final court order — but only the final order. They don't help you prepare for settlement negotiations, calculate tax-adjusted trade-offs, or understand whether a present-value offset or deferred distribution makes more financial sense for your situation. And their fee applies separately to each plan in the marriage — two retirement accounts means two QDRO fees.

This workbook is the preparation system all of them assume you've already done. One purchase, instant download, covers every type of retirement account in one place — and when you do engage a QDRO drafter or attorney, you hand them a complete, organized file instead of starting from scratch at their hourly rate.

100% Satisfaction Guarantee

If this workbook doesn't give you a clearer, more organized path through dividing your retirement accounts, email [email protected] and we'll make it right — no hoops, no time limit.

— Less Than 15 Minutes of a Lawyer's Time

A single hour with a family law attorney costs $300 or more. A QDRO drafter charges $300–$700 per retirement plan. This workbook gives you the entire preparation system — inventory worksheets, valuation calculators, the full QDRO pipeline, IRA transfer rules, tax-trap detection, government pension workflows, and survivor benefit protection — for a fraction of one professional consultation. Start free with the Quick-Start Checklist, or get the complete workbook and walk into your next session prepared.