You Have One Chance to Get This Right

When a 35-year-old divorces and makes a financial mistake, they have three decades of earning power to recover. When you divorce after 50, every dollar lost in the settlement is a dollar that cannot be replaced before retirement.

Standard-of-living declines average 45% for women over 50 after divorce. Among gray-divorced women over 63, 27% live in poverty. These outcomes are not inevitable — they are the downstream result of settlement mistakes that structured preparation can prevent.

The problem is not a lack of information. Free court websites give you blank forms. Attorney consultations cost $300–$550 per hour. Generic divorce guides are built for younger couples splitting a car and a rental lease. None of them address the five irreversible risks that define divorce after 50: retirement account division errors, lost Social Security benefits, health insurance gaps, the house-for-pension trap, and estate plan failures.

The Gray Divorce Navigation System

This is not another divorce checklist. It is a structured financial preparation workspace — 17 chapters and eight standalone printable worksheets that walk you through every high-stakes decision in sequence, from the first private financial audit through post-decree execution. Each worksheet is its own PDF — print it, bring it to a meeting, fill it in by hand.

The guide is built around a single insight: the financial preparation work for a later-life divorce is nearly identical regardless of your state or country. What varies is local law. What does not vary is the strategic sequence — which records to gather, how to evaluate a settlement offer, how to compare pre-tax and post-tax assets, and how to avoid the irreversible mistakes that erase decades of retirement savings.

What's Inside

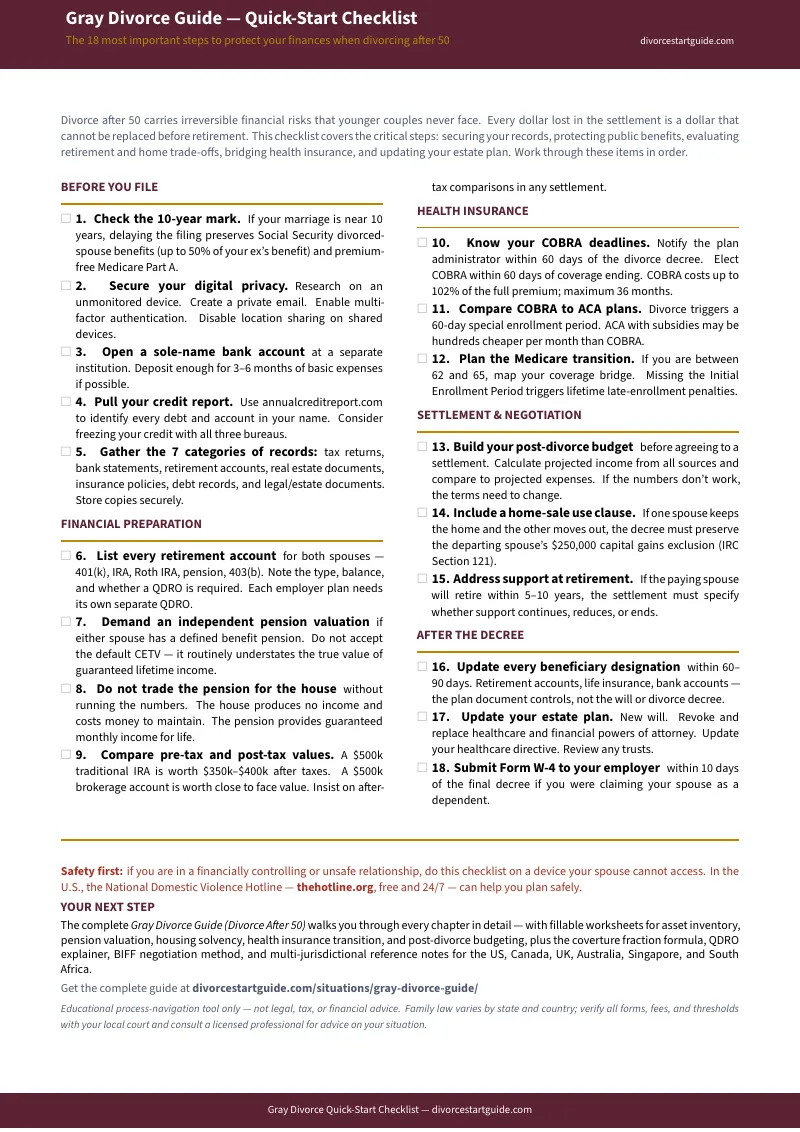

- The 10-Year Rule Chapter — Social Security divorced-spouse benefits can be worth tens of thousands of dollars over your lifetime, and filing one day too early can forfeit them permanently. This chapter explains eligibility, claiming strategies at age 62 vs. full retirement age, and survivor benefits most people never learn about.

- Retirement Account Division — Why a $500,000 traditional IRA is not equal to $500,000 in a brokerage account (the IRA carries 25–30% future tax liability). How 401(k)s, IRAs, 403(b)s, and pensions each require different legal instruments to divide. What a QDRO is, when you need one, and how to avoid the errors that invalidate them.

- Pension Valuation Worksheets — Defined benefit pensions are the most undervalued asset in gray divorce. The coverture fraction formula, lump-sum vs. deferred distribution comparison, and the pension-vs-house trade-off analysis that prevents the second most common gray divorce mistake.

- Health Insurance Transition Planner — COBRA continuation (up to 36 months at 102% of the full premium), ACA marketplace special enrollment (60-day window after divorce), and Medicare enrollment timing to avoid lifetime late-enrollment penalties. Side-by-side cost comparison worksheet.

- The Matrimonial Home Decision Framework — Keep, sell, or buy out — analyzed through carrying costs, refinancing requirements, debt-to-income ratios, and the capital gains tax exclusion rules that change after divorce.

- Spousal Support Analysis — Duration factors, the retirement-age question (what happens to alimony when the payor retires), and the post-2018 tax rules that eliminated the deduction for the payor.

- Tax Rules That Change Everything — Filing status impacts, the difference between pre-tax and post-tax asset valuation, IRA transfer rules (IRC Section 408(d)(6)), and home-sale exclusion deadlines.

- Estate Planning Execution Checklist — The updates most people forget: beneficiary designations on life insurance and retirement accounts (not automatically revoked by divorce in many states), powers of attorney, healthcare directives, and trust amendments — with a 60–90 day post-decree execution timeline.

- Single-Income Retirement Budget Builder — A realistic post-divorce financial plan built from your actual numbers, not generic rules of thumb. Fixed vs. variable expense audit, emergency fund targets, and long-term cash flow projections.

- Mediation and Negotiation Preparation — BIFF communication scripts (Brief, Informative, Friendly, Firm), mediator interview questions, and the 10 most common gray divorce mistakes mapped to the chapters that prevent them.

Who This Guide Is For

- You are considering divorce and want to understand the financial landscape before you involve an attorney or alert your spouse

- You are actively divorcing and need to evaluate a settlement offer, divide retirement accounts, or make the keep-vs-sell decision on the house

- Your divorce is final and you need to execute the post-decree steps — beneficiary updates, health insurance transition, single-income budgeting

- Your marriage is near the 10-year mark and you need to understand the Social Security implications of your filing date

- You are the primary earner and want to understand pension division, QDRO requirements, and how to model trade-offs accurately

Why Free Resources Fall Short

State court self-help pages give you FL-140 and FL-150 with zero explanation of strategy. AARP articles explain the 10-year rule in 400 words but do not give you a worksheet to evaluate your specific situation. Etsy divorce planners offer pretty checklists designed for 30-year-olds splitting a rental deposit. Hello Divorce charges $99–$499 per month and fully supports only eight states.

None of these address the core challenge of gray divorce: the decisions are irreversible, the financial instruments are complex, and the margin for error is effectively zero. A $500,000 pension valued incorrectly, a COBRA deadline missed by a week, or a beneficiary designation left unchanged — any one of these can cost more than a year's worth of retirement income.

This guide gives you the strategic sequence and the worksheets to avoid those mistakes — for less than the cost of 6 minutes with an attorney.

Multi-Jurisdictional Coverage

The guide leads with common United States patterns and includes dedicated reference notes for Canada, the United Kingdom, Australia, Singapore, and South Africa. Throughout every chapter, "Local Law Alert" markers flag exactly where you must verify your own jurisdiction's rules — so you never mistake universal preparation guidance for state-specific legal advice.

100% Satisfaction Guarantee

If the guide does not help you feel more prepared and organized for the decisions ahead, email us for a full refund. No questions, no time limit.

— Less Than 6 Minutes With an Attorney

The average family law attorney charges $300–$550 per hour. A single hour of intake preparation — the kind of financial organizing this guide walks you through in 17 structured chapters — costs more than most people spend on groceries in a week. This guide gives you the same preparation framework for a fraction of one billable increment.

The free checklist gives you the first seven steps. The full guide gives you the complete financial preparation system — 10 PDFs including the guide, the quick-start checklist, and eight standalone worksheets covering asset inventory, retirement account division, pension valuation, housing affordability, health insurance transition, post-divorce budgeting, Social Security eligibility, and estate planning execution — so you walk into your first professional consultation organized, informed, and ready to protect your retirement.