Nevada is a community property state. That means 50/50 — but only if you know what counts.

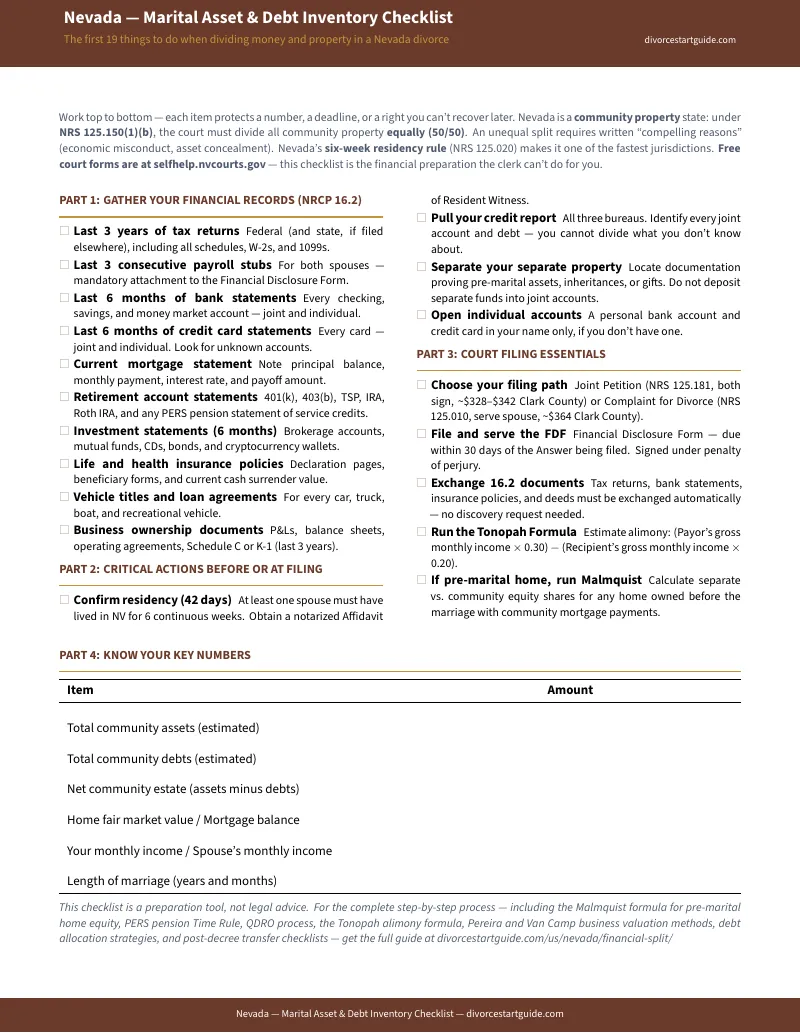

Under NRS 125.150, a Nevada divorce court must divide community property equally. Not "equitably." Not "fairly, as the judge sees fit." Equally. Every dollar earned during the marriage, every debt incurred, every asset acquired — split down the middle.

The trouble is that "community property" and "everything you own" are not the same thing. An inheritance deposited into a joint checking account may have lost its separate identity. A house bought before the marriage with a community-funded mortgage payment has both separate and community equity — and Nevada uses a specific formula (Malmquist v. Malmquist) to calculate the split. A PERS pension earned over twenty years but only twelve during the marriage needs a coverture fraction under NRS 125.155. A joint credit card is community debt even if only one spouse made the charges — and the divorce decree that assigns it won't stop the creditor from coming after you.

The Clark County and Washoe County self-help centers give you every official form for free. The mandatory Financial Disclosure Form must be filed within 30 days of your Answer — signed under penalty of perjury. But nobody at the courthouse will tell you how to classify your assets, calculate your home equity, trace a separate property contribution, or structure a retirement division that doesn't trigger a tax penalty.

The problem isn't finding the forms. It's knowing the numbers to put in them.

You have two options that both cost you:

- Download the free forms — and stare at empty boxes with zero guidance on how to calculate your equity split, value your retirement, or negotiate a debt allocation.

- Hire an attorney — at $300–$500 an hour on top of a $3,000–$10,000 retainer, where the most expensive hours are the ones spent organizing bank statements and explaining basic community property rules you could have learned for yourself.

There's nothing in between. Until now.

The Nevada 50/50 Compliance Method

This guide is built on one idea: the state gives you the empty boxes for free — we give you the math, the formulas, and the Nevada-specific strategy to fill those boxes out correctly before you sign anything or walk into a lawyer's office.

It is not a stack of forms (those are free). It is not generic financial advice. It is a process-navigation and financial-modeling toolkit built specifically around Nevada statutes — the community property mandate of NRS 123.220, the equal-division rule of NRS 125.150, the Malmquist home equity formula, the PERS coverture fraction under NRS 125.155, and the spousal support factors of NRS 125.150(9) — so that every number you bring to the table is defensible, organized, and working for you instead of against you.

For — less than a single hour of an attorney's time — you get the exact worksheets and calculations that make the difference between a fair settlement and one you regret for a decade.

What's inside — and the fear each part solves

- The Community vs Separate Property Classifier — one row per asset, documenting source, acquisition date, commingling events, and current value so you can defend classifications under NRS 123.130 and NRS 123.220. Solves: losing a pre-marital account or inheritance because you couldn't prove it was separate.

- The Malmquist Home Equity Calculator — the exact Nevada Supreme Court formula for splitting appreciation between separate and community interests based on each side's mortgage principal contributions. Plus three structural options (buyout, sell, deferred sale) and a refinance-deadline checklist. Solves: overpaying for a buyout, or losing equity you contributed before the marriage.

- The Financial Disclosure Form Prep Worksheet — mirrors the Clark County and Washoe County FDF line by line, with fill-in guidance for monthly income, expenses, assets, debts, and the mandatory three-paystub attachment. Solves: an adverse judicial inference from a sworn form filled out wrong — or a rejected filing.

- The QDRO & Retirement Division Roadmap — the five-step process for dividing 401(k)s, IRAs, and 403(b) plans without triggering early withdrawal penalties, plus the PERS pension coverture fraction under NRS 125.155 and the offset strategy for trading retirement value against other assets. Solves: accepting a "50/50" retirement split that's really lopsided once taxes and pension rules are counted.

- The Debt Allocation Ledger & Creditor Shield — split community debts 50/50 and classify individual debts, with the warning most people learn too late: a divorce decree dividing debt does not bind your creditors. If your spouse defaults on a joint account, the issuer can still sue you. Includes a 90-day account-transfer timeline and credit-protection checklist. Solves: getting chased for your ex's debt years after the divorce is "final."

- The Spousal Support Factors Worksheet — model your alimony exposure or entitlement using every factor under NRS 125.150(9), including the Tonopah Factors for duration and amount. Solves: not knowing whether you'll pay (or receive) $400 or $2,000 a month, or for how long.

- The After-Tax Negotiation Ledger — value every asset by fair market value, cost basis, and after-tax worth, because a $100,000 brokerage account with a $20,000 basis is worth far less after capital gains than $100,000 in cash. Solves: splitting the estate "evenly" on paper and quietly getting the worse half.

- The Full Nevada Divorce Workflow Map — from the six-week residency requirement through filing, service, FDF exchange, mediation, the Marital Settlement Agreement, QDRO pre-approval, the final hearing, and post-decree transfers. Solves: missing a deadline, skipping a step, or getting blindsided by a procedure nobody mentioned.

Who this is for

- You earn too much to qualify for free legal aid but can't justify draining thousands from the marital estate on billable hours.

- You're representing yourself and need a sequential map from "we need to split everything" to a signed decree.

- You are hiring a lawyer — and want to walk in with your assets classified, your home equity calculated, and your FDF drafted, so you're paying for advocacy, not data entry.

- You have something to protect: a pre-marital home, an inheritance, a PERS pension, a business, or a retirement account you built.

Why not just use the free tools?

Because they stop exactly where the hard part starts.

- Clark County & Washoe County Self-Help Centers (free) give you blank PDF forms and automated interview tools — and staff who are legally prohibited from explaining a single strategic consequence of how you fill them in.

- selfhelp.nvcourts.gov (free) provides state-level court instructions but no worksheets, no home equity formulas, and no retirement division guidance.

- Hello Divorce ($499–$999) and NevadaDivorce.org ($599–$1,299) automate filling out the forms. Neither helps you value a house with the Malmquist formula, calculate a PERS coverture fraction, or model a retirement offset before you commit the numbers.

- QDRO.com ($399) drafts one retirement order and nothing else — no house, no debt, no support, no strategy.

- A private attorney ($3,000–$10,000 retainer) can do all of it — while the meter runs on hours you spend handing over documents you could have organized for .

This guide is the missing bridge: the math and worksheets that let you design a fair, structurally sound agreement first — then fill out the free forms, or hand a mediator or attorney a clean, organized file.

An honest promise

This is an educational financial-organization and process-navigation tool. It is not legal advice, it doesn't represent you in court, and it doesn't pretend a download replaces a lawyer when your case genuinely needs one — it tells you plainly when to bring one in. If your combined gross assets exceed $1 million or either spouse's gross income exceeds $250,000, your case triggers Complex Litigation Procedures and you should consult a licensed attorney.

Try it. Work through the property classifier and the Malmquist calculator. If it doesn't give you more clarity and control over your financial split than anything else you've found, it isn't doing its job — reply to your receipt and we'll make it right.

Start where you are

Not ready for the full guide? Begin free with the Nevada — Marital Asset & Debt Inventory Checklist: a one-page inventory that captures every asset, debt, and property classification in one place — the raw numbers you'll need before you touch the state's mandatory Financial Disclosure Form.

When you're ready to turn that inventory into a settlement — with the Malmquist formula, the PERS coverture math, the spousal support factors, and the after-tax ledger — get the complete Nevada Divorce Financial Split & Asset Division Guide and fill in every box with numbers you can defend.