Tennessee's free court Form 5 comes with a warning most people discover too late.

You found the forms on tncourts.gov — the Complaint, the Marital Dissolution Agreement, the Income and Expense Statement. You sat down to fill them out. And then you read the instructions on Form 5: "This form may NOT be used if either party owns real property, retirement benefits, or a business interest."

That single sentence eliminates everyone with a mortgage, a workplace 401(k), or even a small side business. If you have real assets, Tennessee law requires a custom MDA — and the free forms give you no guidance on how to structure one.

Meanwhile, a family law attorney in Davidson County charges $250–$400 an hour. A $3,500 retainer buys you roughly ten hours. Three of those hours go toward sorting your bank statements into the categories their paralegal needs. That's over $1,000 in document-sorting work you could have done yourself — if someone told you what the categories were and in what order.

You don't need someone to fill in boxes for you. You need to know what the numbers mean before you write them down.

The Tennessee Equitable Distribution Preparation System

This is a complete, step-by-step guide to dividing money and property in a Tennessee divorce — built for the specific statutes, doctrines, and procedural rules that make Tennessee different from every other state. It is not legal representation and it does not file your papers. It is the classification, calculation, and sequencing intelligence that Tennessee's blank forms leave out.

At its core is the Equitable Distribution Preparation System — a structured method that walks you from "I have a pile of bank statements and no idea what's marital vs. separate" to a clean, defensible asset-and-debt inventory that meets the court's standard under T.C.A. § 36-4-121. It handles the part everyone gets wrong: classifying property using the commingling and transmutation doctrines, calculating a home equity buyout that accounts for refinancing costs and the automatic injunction timeline, applying the pension coverture fraction to TCRS and employer plans, allocating debts using the Mondelli and Alford factors, and building a spousal support estimate using the four statutory classes that Tennessee courts actually recognise.

What's inside — the 15-chapter guide, standalone worksheets, and the free checklist

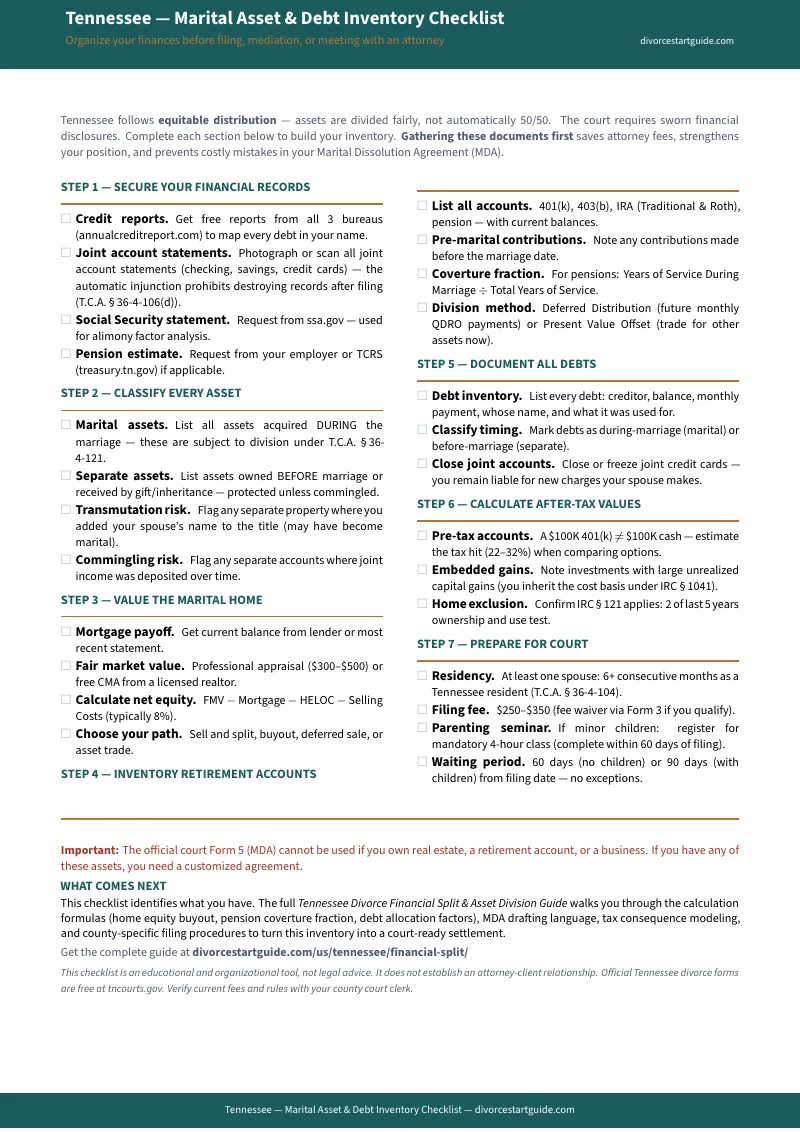

- Marital vs. Separate Property Classification — the tracing method that turns commingled accounts into documented separate-property claims. Because depositing an inheritance into a joint checking account triggers Tennessee's transmutation doctrine — unless you can trace the funds back to their origin with clear and convincing evidence.

- The Document Collection Workflow — exactly which records to gather (three years of tax returns, twelve months of bank statements, current mortgage statements, retirement plan documents, business records) and how to organise them before the automatic statutory injunction under T.C.A. § 36-4-106(d) locks everything in place.

- The Family Home Decision Framework — sell, buyout, or deferred co-ownership? The guide calculates net equity after mortgage, HELOCs, liens, and transaction costs. It covers the refinance-into-one-name requirement, primary-custodian considerations, and capital gains exposure under IRC § 121 if you defer the sale.

- Retirement and Pension Division — coverture fraction math for defined-benefit pensions (including TCRS and military pensions), the QDRO process for employer 401(k)s and 403(b)s, IRA transfer mechanics that avoid early-withdrawal penalties, and the offset strategy for trading retirement claims against home equity.

- The Debt Allocation Method — Tennessee's Mondelli and Alford factors for equitable debt division, the critical distinction between what the court orders and what creditors can still enforce against you on joint accounts, and a credit-freeze action plan for the transition period.

- Spousal Support Analysis — the four classes of alimony under T.C.A. § 36-5-121 (rehabilitative, transitional, in futuro, and in solido), how marital fault affects alimony but not property division, and a temporary support estimation worksheet for mediation preparation.

- Business Valuation Roadmap — enterprise vs. personal goodwill, the marketability and minority discounts, when a formal CBV or ASA appraisal is required, and how to protect operating income from overly aggressive discovery requests.

- Tax Consequences Chapter — IRC § 1041 tax-free transfers, the hidden tax-basis trap ($40,000 in cash vs. $40,000 in a traditional 401(k) are not the same asset), and filing status optimisation for the tax year of divorce.

- MDA Drafting Framework — how to structure a Marital Dissolution Agreement that addresses every asset class, satisfies the chancery court's requirements, and avoids the 180-day expiration trap where an unsigned MDA becomes legally stale.

- Post-Decree Administration Checklist — every deed transfer, title change, beneficiary update, insurance policy change, and account retitling that must happen after the final decree is entered.

Who this is for

The spouse quietly gathering records before filing the Complaint for Divorce. The person staring at Tennessee's Income and Expense Statement with a stack of pay stubs and no idea how to connect the two. The homeowner calculating whether they can afford to keep the house after a refinance at current interest rates. The employee wondering how to split a TCRS pension or a workplace 401(k) without triggering tax penalties. The cooperative couple who want to reach a fair agreement at the kitchen table without spending $10,000 on attorneys — but need the math to prove the deal is actually fair. And the spouse who already has an attorney but wants to stop paying $350 an hour for document organisation they can handle themselves.

Why not just use the free resources?

Because the free resources give you forms, not calculations. Tennessee's tncourts.gov provides Form 5 — a blank Marital Dissolution Agreement with empty boxes that you cannot legally use if you own a house. DivorceNet and Nolo publish educational articles explaining what equitable distribution means in theory. Neither tells you how to calculate a coverture fraction, estimate a home equity buyout, or figure out whether accepting the retirement account or the house gives you a better after-tax position.

The national DIY platforms — 3 Step Divorce at $299, LegalZoom's subscription plans — generate paperwork based on your inputs. They do not show you how to classify commingled property, trace separate assets, or apply the specific Tennessee factors that chancery judges weigh when they review your proposed division. They fill in the boxes. This guide tells you what the right numbers are before you write them down.

An honest guarantee

Work through the Equitable Distribution Preparation System. If the guide doesn't make your financial split clearer and better organised than any blank form or free article could — email us within 30 days for a full refund. The risk of trying it is a fraction of one attorney billable hour. The risk of guessing on your asset division is measured in years of financial consequences.

For — less than fifteen minutes of attorney time — you get the classification system, the coverture math, the worksheets, and the step-by-step sequence that Tennessee's free forms leave out.

Stop staring at blank boxes and fine-print warnings. Get the guide, build your inventory, and walk into your divorce with the numbers already done.