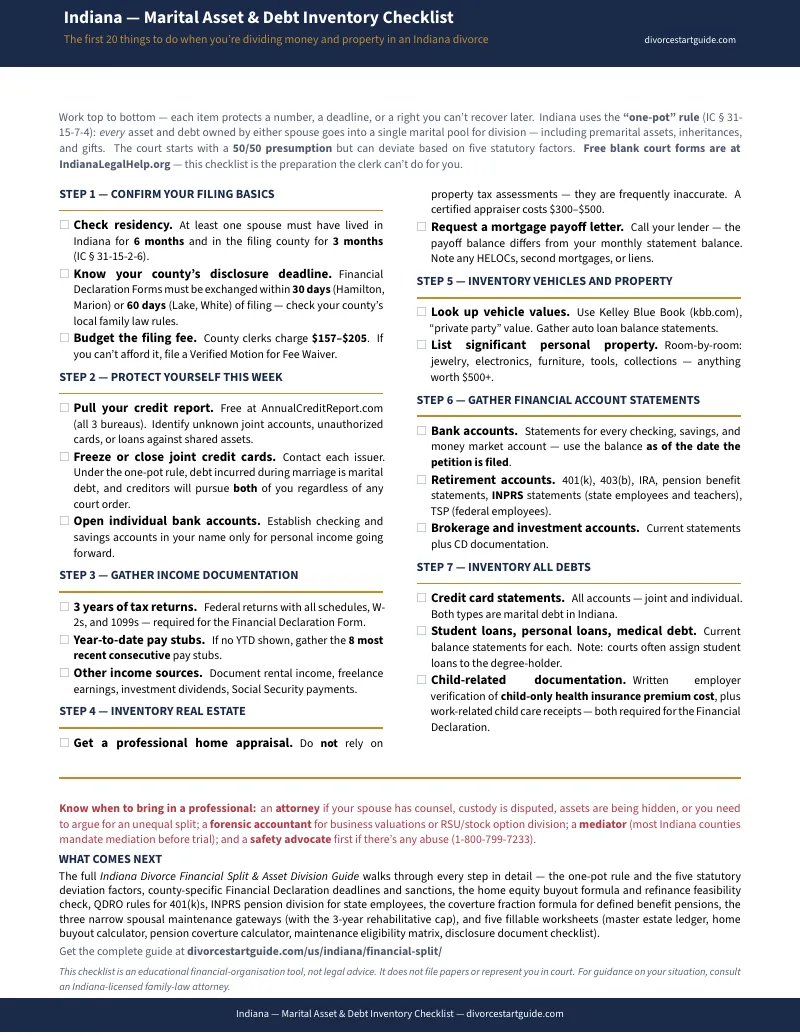

The court forms ask you to list everything you own. They don't tell you how to figure out what it's worth or how to split it.

You've found the Verified Financial Declaration Form — the one Lake, Marion, and Hamilton counties require you to complete under penalty of perjury within 45 to 60 days of filing. It asks for the value of every bank account, every retirement plan, every piece of real estate. It asks for three years of tax returns and your most recent pay stubs. And it gives you blank boxes.

No instructions on how to calculate the fair market value of your home minus the remaining mortgage. No explanation of how Indiana's "one-pot" rule pulls your premarital inheritance into the divisible estate — and what you need to argue to get it back. No guidance on whether keeping the house or trading it for the 401(k) leaves you better off after taxes. Just boxes.

An attorney in Indianapolis charges $250 to $450 an hour. A $3,500 retainer buys you roughly ten hours. Three of those hours go to a paralegal sorting through your bank statements and pay stubs. That's over $1,000 in administrative work you could have done yourself — if someone had shown you the categories.

The Indiana One-Pot Financial Navigation System

This guide is a step-by-step financial preparation system built for the specific rules that make Indiana different from every other state. It does not provide legal advice and it does not file your papers. It gives you the calculation tools, the sequencing, and the worksheets that the blank forms leave out.

At its core is the One-Pot Financial Navigation System — a structured method that walks you from a pile of bank statements and no idea what's divisible to a clean, defensible asset-and-debt inventory that meets the court's standards under IC 31-15-7-5. It covers the part everyone gets wrong: understanding that Indiana has no legal "separate property" at filing, applying the coverture fraction to split pensions, running the refinance feasibility math on the family home, tracing premarital assets through commingled accounts, and building a spousal maintenance assessment using the three narrow gateways that Indiana law actually allows.

What's inside — the 10-chapter guide, 7 standalone worksheets, and the free checklist

- The One-Pot Rule Explained — how Indiana pools every asset into a single marital estate, the presumptive 50/50 split, and exactly how to invoke the five statutory deviation factors when a 50/50 split is unfair. Because understanding this rule is the difference between losing your inheritance and keeping it.

- Financial Disclosure Prep System — which documents to gather (three years of tax returns, recent pay stubs, six months of bank and retirement statements), how to organise them to match what the Verified Financial Declaration Form actually asks for, and county-specific deadline rules so you never miss a filing window.

- Master Marital Estate Ledger — a fillable worksheet to inventory every asset and debt with current fair market values. Models both 50/50 and unequal split scenarios so you can see the equalization payment before you walk into negotiation.

- Home Equity & Refinance Feasibility Calculator — buyout, sell, defer, or offset? The worksheet calculates net equity after mortgage, HELOCs, and transaction costs, then runs a refinance qualification check on a single income. Covers capital gains exposure and the three non-negotiable steps for any buyout.

- Pension Coverture Fraction Calculator — coverture math for defined-benefit pensions, the QDRO process for 401(k)s, and the specific rules for Indiana Public Retirement System (INPRS) pensions. Includes the offset strategy for trading retirement claims against home equity or other assets.

- Spousal Maintenance Eligibility Assessment — Indiana does not have traditional alimony. The worksheet walks you through the three narrow statutory gateways under IC 31-15-7-2: incapacity, caregiver, and rehabilitative (capped at three years). Maps your situation to the eligibility criteria so you know your exposure or entitlement before mediation.

- Debt Division & Creditor Protection Planner — the one-pot rule applies to liabilities too. A standalone worksheet covering the critical distinction between what the court orders and what creditors can still enforce, joint credit card freeze strategy, refinancing timelines, and indemnification clauses that actually protect you.

- Tax Chapter — IRC §1041 tax-free transfers, the hidden tax basis trap (a $40,000 brokerage account and $40,000 in a traditional 401(k) are not the same after taxes), and how the post-2018 TCJA rules eliminated the maintenance payment deduction.

- Settlement Agreement Checklist — common trade-offs, non-adversarial communication scripts, and a comprehensive checklist covering every item your settlement agreement must address — from tax exemption allocation to beneficiary redesignation deadlines.

- Financial Disclosure Document Checklist — every document the Verified Financial Declaration Form requires, organized by category — income, real estate, vehicles, financial accounts, retirement, debts, insurance, and child-related expenses.

Who this is for

The spouse quietly researching before filing. The person staring at a Verified Financial Declaration Form and a shoebox of bank statements with no idea how to connect the two. The homeowner in Hamilton County wondering whether they can afford to keep the house after refinancing on one income. The state employee trying to figure out what happens to their PERF pension. The cooperative couple who want to settle at the kitchen table without spending $15,000 on attorneys — but need the math to prove the deal is actually fair. And the spouse who already has a lawyer but wants to stop paying $350 an hour for document organisation they can handle themselves.

Why not just use the free resources?

Because the free resources give you forms, not calculations. Indiana Legal Help provides blank PDFs. The Indiana Bar Foundation provides a general overview of your rights. Neither one tells you how to calculate a coverture fraction, estimate a home equity buyout, or figure out whether taking the retirement account or the house leaves you better off after taxes.

The national DIY platforms — 3StepDivorce at $299, Divorce.com starting at $499 — generate standardised forms from a questionnaire. They don't cover Indiana's one-pot theory, they don't reference the Verified Financial Declaration Form or the INPRS pension rules, and they don't help with the specific financial calculations that Indiana courts expect to see in a settlement proposal.

An honest guarantee

Work through the One-Pot Financial Navigation System. If the guide doesn't make your financial split clearer and better organised than any blank form or free article could — email us within 30 days for a full refund. The risk of trying it is a fraction of one attorney billable hour. The risk of guessing on your asset division is measured in years of financial consequences.

For — less than fifteen minutes of attorney time — you get the one-pot classification system, the coverture math, the worksheets, and the step-by-step sequence that the free forms leave out.

Stop staring at blank boxes. Get the guide, build your inventory, and walk into your divorce with the numbers already done.