Your divorce decree is signed. Nobody told you what comes next takes longer than the divorce itself.

The Circuit Court signed your Judgment of Absolute Divorce. The marriage is over. And now you're staring at a stack of life admin that nobody prepared you for: a Social Security card in the wrong name, joint bank accounts your ex can still drain, a 401(k) that still names them as beneficiary, a mortgage with both names on it, and a will that leaves everything to the person you just divorced.

Each agency has its own forms, its own fees, its own processing timeline — and a strict dependency order that nobody tells you about. Update your driver's license at the MVA before Social Security and the MVA system rejects you. Submit a QDRO to the court before the plan administrator pre-approves it and the judge sends it back. Record a quitclaim deed without checking whether your lender triggers a due-on-sale clause and you have a new problem entirely.

Maryland's 2023 family law reforms made getting divorced faster — mutual consent, six-month separation, irreconcilable differences. But the post-divorce administrative maze is exactly as complex as it was before. An attorney will guide you through it — at $200–$425 an hour. Three of those hours go to explaining MVA procedures and SSA form requirements. That's $600–$1,275 in administrative hand-holding you can handle yourself — if someone gives you the sequence.

The Maryland Post-Divorce Sequencing System

This is a complete, step-by-step guide to every administrative task after a Maryland divorce — built around the one thing that free forms and generic checklists get wrong: the dependency order.

At its core is the Post-Divorce Sequencing System — a structured method that walks you through the exact order of federal, state, county, and private-institution updates so nothing gets rejected and nothing falls through the cracks. It handles the part everyone gets stuck on: knowing that SSA must come before the MVA, that plan administrator pre-approval must come before court filing, that HB 1018 lets you assume a conventional mortgage instead of refinancing, that Maryland Estates and Trusts Code § 4-105 revokes will provisions but not trust provisions, and that beneficiary designations on federal plans follow federal law even after a Maryland divorce.

What's inside — the 12-chapter guide, worksheets, and the free checklist

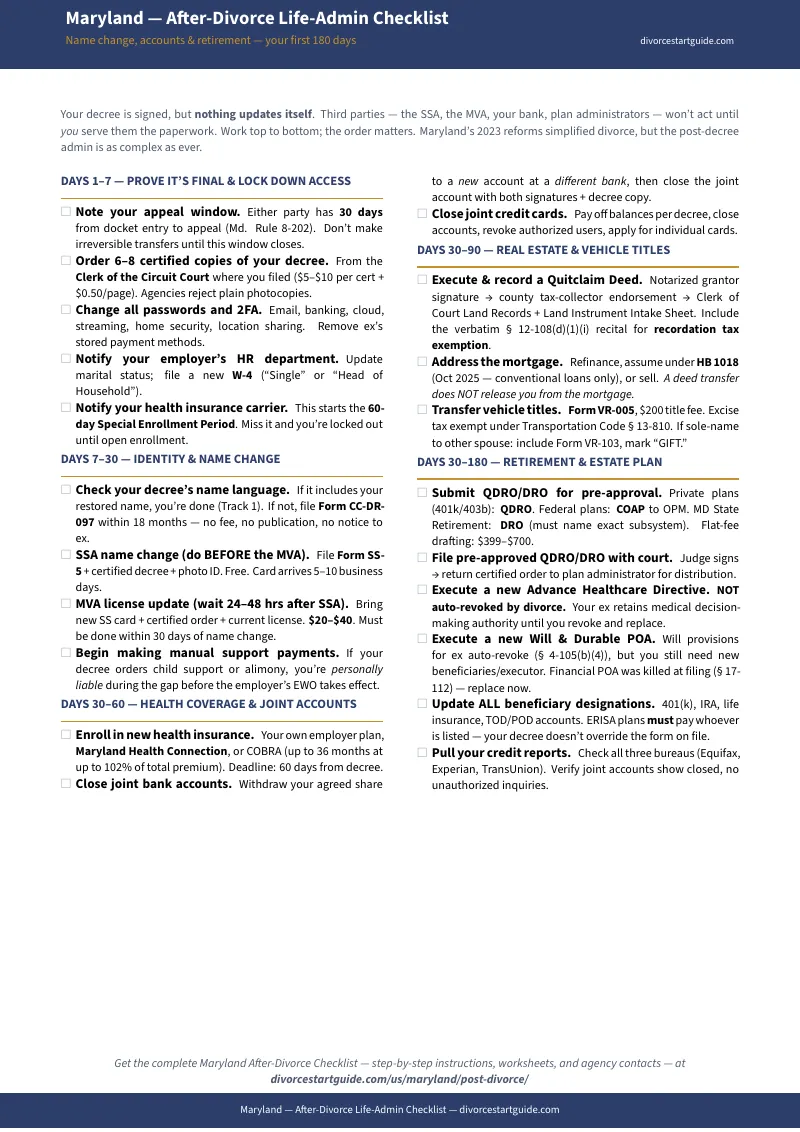

- Decree Verification and Certified Copies — how many certified copies to order (6–8 minimum), where to get them, county-by-county certification fees ($5–$10 plus $0.50/page), and the 30-day appeal window under Maryland Rule 8-202 that determines which tasks you can start immediately and which must wait.

- The Name Change — Three Legal Tracks — Track 1: built into the decree (no extra filing). Track 2: simplified motion within 18 months via Form CC-DR-097 (no filing fee, no newspaper publication, no notice to your ex since January 2024). Track 3: separate civil petition after 18 months via Form CC-DR-060 ($165 filing fee, mandatory newspaper publication, 30-day waiting period). The guide covers all three plus the SSA → MVA → passport dependency chain.

- Joint Account Separation and Credit Protection — under Maryland Financial Institutions Article § 1-204(f), any party on a joint account has absolute right of withdrawal. Your ex can legally empty the account before you act. The guide covers a bank-by-bank action plan, credit freeze procedures at all three bureaus, authorized user removal, and Maryland's dissipation standard for one-sided withdrawals during separation.

- Real Estate Transfer and the HB 1018 Mortgage Assumption — a quitclaim deed transfers ownership but does not release the departing spouse from the mortgage. House Bill 1018 (effective October 2025) now requires conventional mortgage lenders to allow assumption at the original rate. The guide covers the assumption process, the FHA/VA/USDA exemptions, the recordation and transfer tax exemption under Tax-Property Code § 12-108(d), and what to do when your lender claims the law doesn't apply.

- Vehicle Title Transfers at the MVA — the MVA treats spousal transfers as full title transfers ($200 fee). Joint-to-sole consolidation is excise-tax-exempt. Sole-to-sole transfers require Form VR-103 with "GIFT" in the sale price field. The guide covers both scenarios, the Transportation Code § 13-810 exemptions, and the $240 duplicate title fee if the original is missing.

- QDRO and Retirement Division — Private Plans, State Pensions, TSP — ERISA-governed plans (401(k), 403(b), private pensions) require a Qualified Domestic Relations Order. Maryland state and municipal pensions, the federal Thrift Savings Plan, and military retirement use a DRO or COAP. The guide covers the pre-approval workflow, the offset vs. shared-interest strategy, tax-free rollover rules, and the deadline risk: if your ex retires or withdraws before the order is qualified, the money may be gone.

- Estate Plan Overhaul — Maryland Estates and Trusts Code § 4-105(b)(4) revokes will provisions benefiting your ex-spouse. It does not revoke revocable trust provisions, trustee appointments, or bequests to your ex's relatives. Federal employee plans (FEGLI, TSP, SGLI) follow federal law. The guide includes a beneficiary audit worksheet covering every account type.

- Health Insurance Transition — COBRA election (60 days to elect, 45 days to pay first premium, up to 36 months at 102% of total premium), Maryland Health Connection marketplace enrollment, employer plan options, and the cost comparison worksheet.

- Child Support and Alimony Transitions — the gap between the decree and the Earnings Withholding Order, manual payment obligations, modification procedures, and what happens if your ex falls behind.

- Tax Filing and Withholding Changes — filing status transitions, the federal rule making post-2018 alimony tax-neutral, W-4 updates, dependent exemption rules, and the capital gains trap on deferred property sales.

- Utility Accounts and Everyday Admin — address changes, utility account transfers, subscription cancellations, and the digital account separation checklist.

- When to Get Professional Help — when a QDRO preparer ($399–$700 flat fee) makes more sense than doing it yourself, when you need a forensic accountant ($1,500–$3,500 for tracing), and when the answer is an attorney, not a worksheet.

8 standalone printable worksheets — take them to the bank, the MVA, and the courthouse

- Name Change Tracker — all three legal tracks side by side, plus the SSA → MVA → passport dependency chain as a step-by-step checklist

- Joint Account Separation Worksheet — bank-by-bank action plan, credit card closure tracker, three-bureau credit freeze steps, and credit report verification

- Real Estate Transfer Checklist — quitclaim deed steps, recordation and transfer tax exemptions, and the HB 1018 mortgage assumption decision

- Vehicle Title Transfer Reference — MVA forms, fees, excise tax exemptions by scenario, and auto insurance updates

- Retirement Division Workflow — QDRO, DRO, and COAP lifecycle from plan documents through distribution, with the marital share formula and cost guide

- Beneficiary Audit Worksheet — what Maryland law automatically revokes vs. what you must update manually, plus the post-divorce estate planning action list

- 90-Day Action Plan — week-by-week timeline with checkboxes, the agency directory, and the forms reference on a single two-page sheet

- Health Insurance Comparison — COBRA vs. Maryland Health Connection vs. employer plan side-by-side, with a fillable cost comparison table

Who this is for

The person staring at a signed divorce decree and a list of accounts, IDs, and titles that still have the wrong name on them. The newly single person who needs to separate joint finances before the ex drains the checking account. The state employee who's been told they need a DRO for their pension and has no idea what that means or how much it should cost. The homeowner who wants to keep the house under HB 1018's mortgage assumption option instead of refinancing at a higher rate. And the person with an attorney who wants to stop paying $300 an hour for someone to explain how the MVA works.

Why not just use the free resources?

Because the free resources give you forms, not sequences. The Maryland Judiciary self-help portal provides Form CC-DR-097 for name restoration — but doesn't tell you that the MVA will reject your application if SSA hasn't synced yet. The Social Security Administration tells you what to bring to their office — but doesn't tell you to wait 24–48 hours before visiting the MVA. Your retirement plan's Summary Plan Description explains the QDRO process — but doesn't warn you about the pre-approval workflow or the withdrawal risk.

The information exists across dozens of disconnected government websites, each one accurate for its own agency and silent about every other agency. This guide connects the dots into one sequenced workflow so you don't spend weeks bouncing between agencies that each point you somewhere else first.

An honest guarantee

Work through the Post-Divorce Sequencing System. If the guide doesn't make your post-divorce administration clearer and faster than any blank form or free article could — email us within 30 days for a full refund. The risk of trying it is a fraction of one attorney billable hour. The risk of missing a beneficiary designation, a QDRO deadline, or a credit freeze is measured in years of financial consequences.

For — less than fifteen minutes of attorney time — you get the 12-chapter guide, 8 standalone printable worksheets, the 90-day action plan, and the free quick-start checklist. That's 10 PDFs covering every post-divorce task the free forms leave out.

Stop bouncing between agencies. Get the guide, work the sequence, and clear your post-divorce to-do list in weeks instead of months.