The government gives you blank forms. It doesn't give you a math tutor.

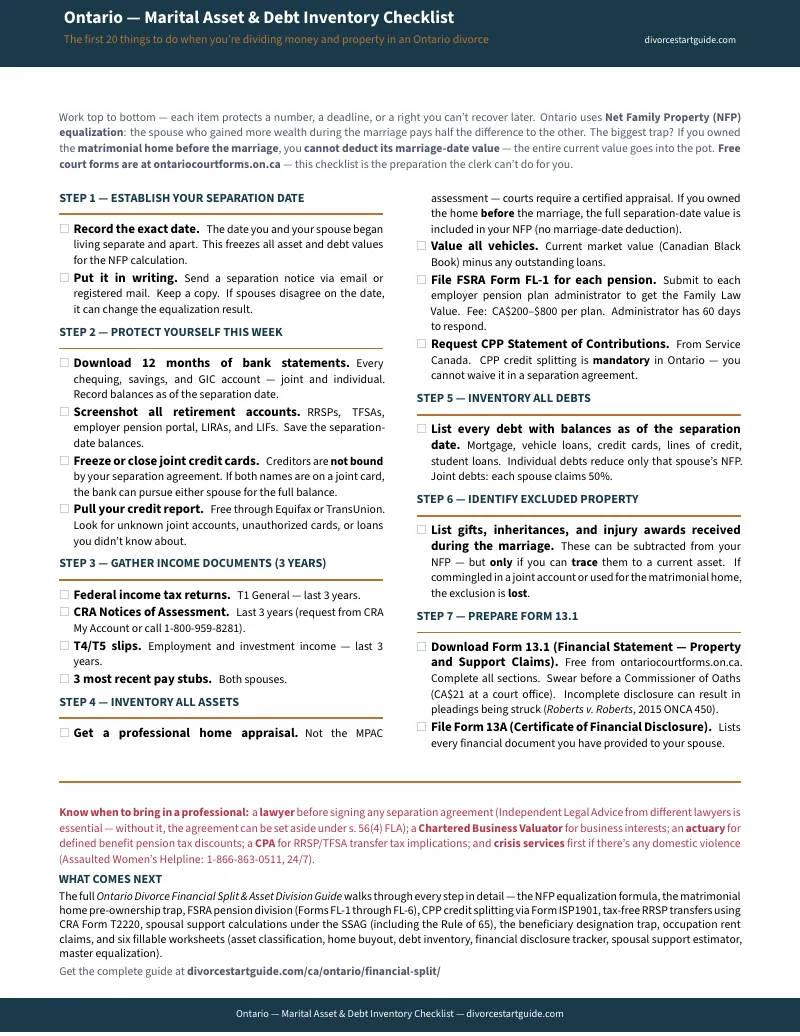

You've downloaded Ontario Court Form 13.1 — the Financial Statement — and you're staring at rows that ask for the fair market value of every asset, every debt, every monthly expense, all under oath. But the form doesn't tell you how to calculate your Net Family Property. It doesn't explain that the matrimonial home you owned before marriage can't be deducted from your NFP — a rule that can swing the equalization payment by hundreds of thousands of dollars. And it doesn't warn you that listing your RRSP at face value, without discounting for the income tax you'll owe on withdrawal, will skew the entire calculation against you.

Meanwhile, an Ontario family lawyer charges $350 to $650 per hour. A $2,500 retainer buys you about six hours. Two of those will go to sorting your bank statements, CRA Notices of Assessment, and pay stubs into categories. That's over $800 in administrative work you could have done yourself — if someone had shown you how it all connects.

You don't need someone to fill in the boxes. You need to understand the numbers before you write them down.

The NFP Equalization Navigation System

This is a complete, step-by-step guide to dividing money and property in an Ontario divorce — built for the specific rules that make this province different from every other jurisdiction in North America. It is not legal representation and it does not file your papers. It is the calculation and sequencing intelligence that the blank court forms leave out.

At its core is the NFP Equalization Navigation System — a structured method that walks you from "I have a pile of bank statements and no idea what's shared versus what I keep" to a clean, defensible financial inventory that meets the equalization standard under Ontario's Family Law Act. It handles the parts everyone gets wrong: applying the Section 18 matrimonial home rule, tracing excluded property like inheritances to prove they stay yours, splitting FSRA-regulated pensions correctly, discounting RRSPs for contingent taxes, and preparing a sworn Form 13.1 that won't get challenged.

What's inside — 15 chapters, 3 appendices, standalone worksheets, and the free checklist

- Net Family Property Equalization — the complete NFP formula, explained line by line. How to calculate assets on the separation date, deduct marriage-date values, handle excluded property under Section 4(2), and determine who owes the equalization payment and how much.

- Asset Classification System — every type of property (bank accounts, investments, RRSPs, TFSAs, real estate, vehicles, business shares) classified into the right NFP category. Includes the distinction between married spouses (who get equalization) and common-law partners (who don't under the FLA).

- The Matrimonial Home Chapter — Section 18 of the Family Law Act strips your right to deduct the marriage-date value of the matrimonial home. This single rule can transfer hundreds of thousands of dollars of pre-marital equity to your spouse. The guide walks through how the rule works, when vacation properties also qualify, and your three options: buyout, sale, or exclusive occupation order.

- Form 13.1 Preparation — a section-by-section walkthrough for completing Ontario's Financial Statement, plus a document-gathering checklist covering three years of tax returns, CRA Notices of Assessment, twelve months of bank and credit card statements, mortgage balances, and group benefit statements.

- Pension and Retirement Division — step-by-step instructions for the FSRA pension valuation process (Statement of Family Law Value, fees up to $600 plus HST for defined benefit plans), RRSP transfers using CRA Form T2220, TFSA division, and CPP credit splitting through Service Canada (Form ISP1901).

- RRSP Tax Discounting — why listing pre-tax retirement assets at face value in your NFP overstates their real value, how to apply a 15–25% contingent tax discount, and when you need an actuary for the calculation.

- Debt Allocation — how debts reduce your individual NFP, the critical difference between what a separation agreement says and what creditors can still enforce against you, joint credit card strategy, and mortgage refinancing.

- Hidden Assets and Enforcement — red flags that suggest undisclosed property, tracing methods for cryptocurrency and cash businesses, and the legal penalties under the FLA for incomplete financial disclosure.

- Spousal Support Modelling — entitlement factors, the Spousal Support Advisory Guidelines (SSAG) formulas for both "with child support" and "without child support" scenarios, duration ranges, and the tax treatment of support payments.

- The Beneficiary Designation Trap — why your ex-spouse may still be named on your life insurance, RRSP, pension, and TFSA beneficiary designations, and exactly how to update each one after separation.

- Master Equalization Worksheet — the final calculation. Input every asset and debt value, apply the classification, and calculate the equalization payment needed to settle your property division.

Every worksheet is included as a standalone printable PDF — asset classification, home equity buyout calculator, financial disclosure tracker, pension division checklist, debt inventory, and spousal support estimator. Print the ones you need and bring them to mediation, your lawyer review, or the kitchen table.

Who this is for

The spouse quietly gathering records before filing. The person staring at Form 13.1 and a stack of CRA Notices of Assessment with no idea how to connect the two. The public servant wondering how their OMERS or OPTrust pension gets split. The homemaker calculating whether they can afford to keep the house after refinancing. The cooperative couple who want to reach a fair deal at mediation without spending $5,000 on billable hours — but need the math to prove the deal is actually fair. And the spouse who already has a lawyer but wants to stop paying $500 an hour for document organisation they can handle themselves.

Why not just use the free resources?

Because the free resources give you forms, not calculations. Steps to Justice and CLEO provide excellent legal explanations and guided pathways. The Family Law Information Centres offer guidance. But none of them provide interactive worksheets, step-by-step pension division instructions, or a structured equalization calculation framework. They explain the law — they don't help you calculate your specific financial division.

The national platforms — LegalZoom, Rocket Lawyer, Untie the Knot at $499 to $899 per package — don't know about Ontario's unique NFP system, the Section 18 matrimonial home trap, the FSRA pension process, or the specific sections of the Family Law Act that determine how your assets get classified. Generic separation agreement templates can be set aside by a judge under Section 56(4) if they lack full financial disclosure or Independent Legal Advice.

An honest guarantee

Work through the NFP Equalization Navigation System. If the guide doesn't make your financial split clearer and better organised than any blank form or free article could — email us within 30 days for a full refund. The risk of trying it is a fraction of one attorney billable hour. The risk of guessing on your asset division is measured in years of financial consequences.

For — less than five minutes of attorney time at Ontario rates — you get the classification system, the pension division instructions, the worksheets, and the step-by-step sequence that the free forms leave out.

Stop staring at blank boxes. Get the guide, build your inventory, and walk into your divorce with the numbers already done.