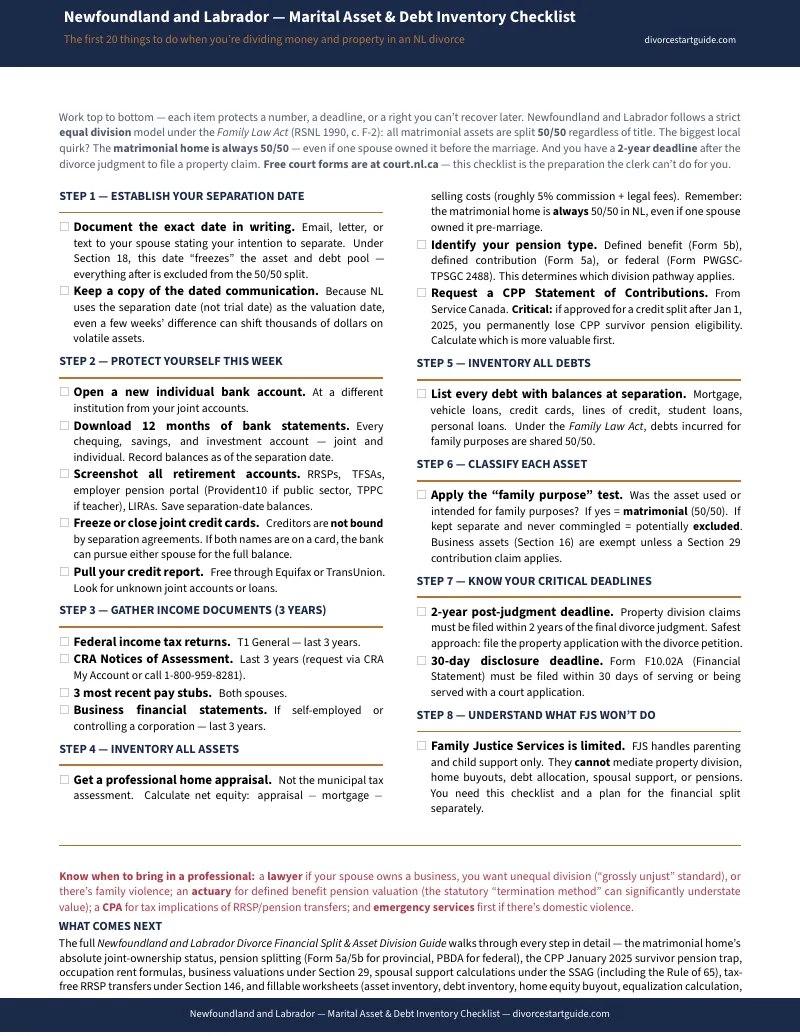

The court gives you blank forms. It doesn't give you a calculator.

You've downloaded Form F10.04A — the Property Statement — from the Supreme Court of Newfoundland and Labrador. Twelve pages of boxes asking for the fair market value of every asset, every debt, every financial interest in your marriage, all under oath. But the form doesn't tell you how to calculate the numbers. It doesn't explain that the matrimonial home you owned before the marriage is still split 50/50 — an absolute rule that overrides the normal pre-marriage exclusion and can swing your settlement by hundreds of thousands of dollars. And it doesn't warn you that choosing a lump-sum pension transfer instead of Form P2 limited-member registration could cost you tens of thousands in understated value.

Meanwhile, a family lawyer in St. John's charges C$150 to C$500 per hour. A C$3,000 retainer buys you roughly eight hours. Two of those will go to sorting your bank statements, CRA Notices of Assessment, and pension plan summaries into categories. That's C$750 in administrative bookkeeping you could have done yourself — if someone had shown you how the pieces connect.

Family Justice Services handles parenting arrangements and child support. Property division, the matrimonial home, pension splitting, and spousal support? That's not their jurisdiction. You walk out of FJS mediation and realize the biggest financial decisions of your separation are still completely unresolved.

You don't need someone to fill in boxes. You need to understand the math before you write anything down.

The Matrimonial Asset Navigation System

This is a complete, step-by-step guide to dividing money and property in a Newfoundland and Labrador divorce — built for the specific rules that make this province different from every other jurisdiction in Canada. It is not legal representation and it does not file your papers. It is the calculation and sequencing intelligence that the blank court forms leave out.

At its core is the Matrimonial Asset Navigation System — a structured method that walks you from "I have a pile of bank statements and no idea what's matrimonial versus what I keep" to a clean, defensible financial inventory that meets the 50/50 equal division standard under the Family Law Act (RSNL 1990, c. F-2). It handles the parts everyone gets wrong: applying the absolute joint-ownership rule for the matrimonial home, tracing excluded property like inheritances to prove they stay yours, splitting pensions correctly under the Pension Benefits Act, understanding the critical January 2025 CPP survivor pension trap, and preparing a sworn Form F10.04A that won't get challenged.

What's inside — 14 chapters, 3 appendices, standalone worksheets, and the free checklist

- Matrimonial Asset Classification — every type of property (bank accounts, investments, RRSPs, TFSAs, real estate, vehicles, business shares) classified into the three NL categories: matrimonial assets, excluded property, and business assets under Sections 16 and 20 of the Family Law Act.

- The Matrimonial Home Chapter — Part I of the Act gives both spouses an absolute 50% ownership interest regardless of who held title before the marriage. This single rule can transfer the full pre-marital equity of a home to the non-owning spouse. The guide walks through how it works, the restriction on unilateral sale or encumbrance, and your three options: buyout, sale, or deferred sale order.

- Excluded Property Tracing — inheritances, pre-marriage bank balances, and third-party gifts are exempt from division only if you can trace them. The guide provides a step-by-step tracing worksheet and explains exactly how commingling destroys the exclusion.

- Pension and Retirement Division — the choice between lump-sum commuted value transfer (termination method, often undervaluing the pension) and Form P2 limited-member registration (deferred pension, often significantly more valuable). Includes the Teachers' Pension Plan Section 17 process, federal PBDA rules, RRSP tax-free rollovers, and CPP credit splitting via Form ISP-1901.

- The 2025 CPP Survivor Pension Trap — any credit split approved on or after January 1, 2025 permanently disqualifies you from receiving a CPP survivor pension from that spouse. The guide explains who this affects most and how to evaluate the trade-off before filing.

- Form F10.04A Preparation — a section-by-section walkthrough for completing the Supreme Court's Property Statement. Document-gathering checklist covering three years of CRA Notices of Assessment, twelve months of bank and credit card statements, mortgage balances, pension statements, and vehicle appraisals.

- Debt Settlement Ledger — compile all joint and separate liabilities, understand that lenders are not bound by your separation agreement, plan joint account closures, and structure mortgage refinancing.

- Business Valuation Framework — EBITDA normalization for owner-operator businesses, the enterprise vs. personal goodwill distinction, share sale with Lifetime Capital Gains Exemption (LCGE) purification, and structured promissory note options.

- Spousal Support Modelling — compensatory and non-compensatory entitlement, Spousal Support Advisory Guidelines (SSAG) formulas for both "with children" and "without children" scenarios, duration ranges, and tax treatment.

- Master Settlement Worksheet — input every asset and debt value, apply the classification, and calculate the equalization needed to reach a fair 50/50 division.

Every worksheet is included as a standalone printable PDF — asset classification worksheet, equalization calculation worksheet, home buyout calculator, pension division decision matrix, excluded property tracing log, debt settlement ledger, spousal support estimator, Form F10.04A preparation checklist, and transfer execution checklist. Print the ones you need and bring them to mediation, your lawyer's office, or the kitchen table.

Who this is for

The self-represented filer staring at a blank Form F10.04A with a stack of bank statements and no idea how to classify them. The parent who completed Family Justice Services mediation and just learned that nobody covered the house, the pension, or the credit card debt. The spouse preparing for a first intake with a private mediator and wanting to stop the C$300-per-hour clock from running on basic document sorting. The financially anxious partner who needs to quietly reconstruct the family balance sheet before formal negotiations begin. And the spouse who already has a lawyer but wants to stop paying C$350 per hour for bookkeeping they can handle themselves.

Why not just use the free resources?

Because free resources give you forms, not calculations. PLIAN's Uncontested Divorce Guide is excellent — but it only applies after all property, debt, and support issues have already been fully resolved through a separate agreement. The Supreme Court website provides Form F10.04A as a blank PDF with no calculation framework attached. Court staff are legally barred from offering advice on how to complete it. Family Justice Services mediators cannot touch property division or spousal support.

The national document builders — LawDepot, CompleteCase — don't know about the absolute matrimonial home rule, the Form P2 limited-member pension registration process, or the "grossly unjust or unconscionable" standard that makes unequal division orders exceedingly rare in this province. Generic templates written for Ontario's NFP system or British Columbia's excluded-property appreciation rules will give you the wrong answer in Newfoundland and Labrador.

An honest guarantee

Work through the Matrimonial Asset Navigation System. If the guide doesn't make your financial split clearer and better organised than any blank form or free article could — email us within 30 days for a full refund. The risk of trying it is a fraction of one attorney billable hour. The risk of guessing on your asset division is measured in years of financial consequences.

For — less than five minutes of attorney time at St. John's rates — you get the classification system, the pension division instructions, the worksheets, and the step-by-step sequence that the free forms leave out.

Stop staring at blank boxes. Get the guide, build your inventory, and walk into your divorce with the numbers already done.