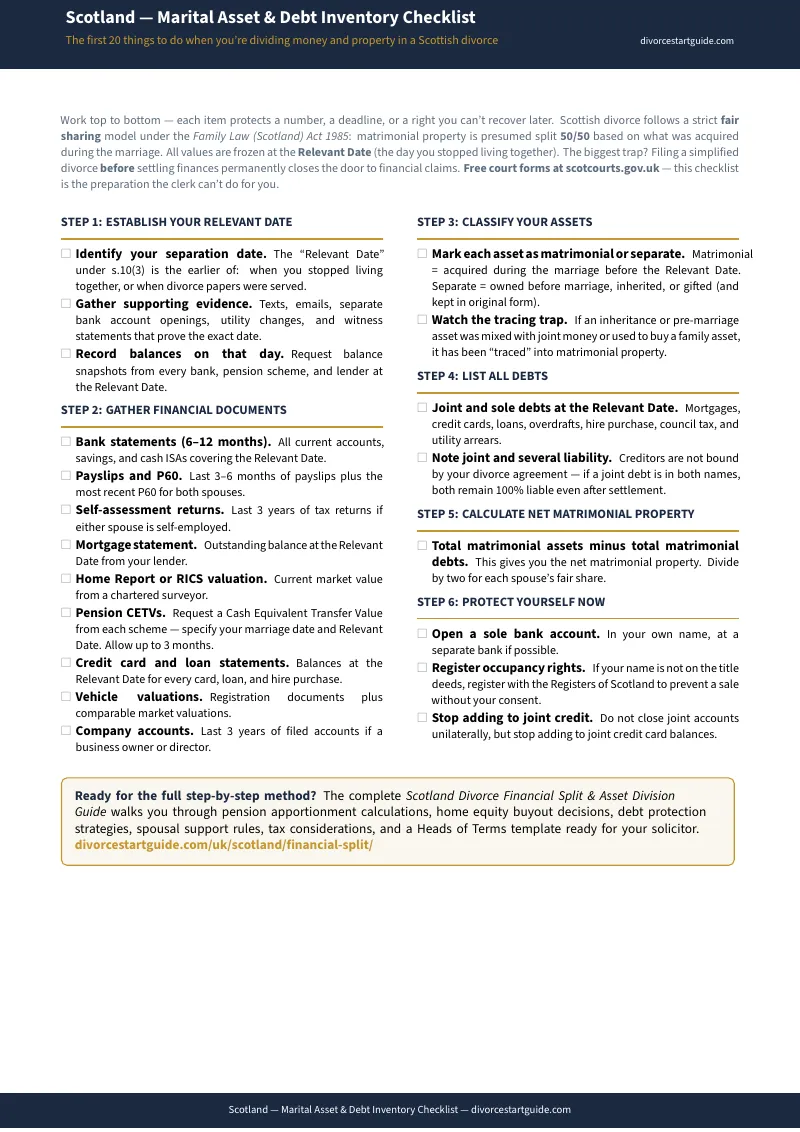

Mygov.scot gives you blank forms. It doesn't tell you how to calculate what belongs in the shareable pool.

You've found the simplified divorce application on the Scottish Courts website — Form A or Form B. And you've hit the warning printed right on page one: "You cannot use this procedure if there are any financial matters outstanding between you and your spouse." That means you need to resolve everything — the house, the pensions, the joint account, the debts — before you can even file. And the forms don't tell you how.

Meanwhile, a family law solicitor in Edinburgh charges £200–£400 per hour plus VAT. A £250 initial consultation buys you forty-five minutes. Half of that goes to organising documents their trainee could have sorted — if someone had told you what to bring and how to categorise it.

You don't need someone to fill in forms for you. You need to know what counts as matrimonial property, how to value it at the relevant date, and how to turn that into a proposal your spouse can sign before you spend thousands on contested proceedings.

The Fair Sharing Navigation System

This is a complete, step-by-step guide to dividing money and property in a Scottish divorce — built entirely around the Family Law (Scotland) Act 1985 and the rules that make Scotland fundamentally different from England and Wales. It is not legal advice and it does not file your papers. It is the calculation and sequencing intelligence that blank government forms leave out.

At its core is the Fair Sharing Navigation System — a structured method that walks you from "I have a pile of bank statements and no idea what's matrimonial" to a clean, documented asset-and-debt inventory that satisfies the court's "fair sharing" standard under Section 10. It handles the part everyone gets wrong: establishing and documenting the relevant date, tracing non-matrimonial property through mixed accounts, applying the pension apportionment formula to calculate the matrimonial share of your CETV, evaluating a family home buyout against the real costs (LBTT, mortgage discharge, re-registration), and building a spousal aliment estimate using the Section 9 principles courts actually apply.

What's inside — 15 chapters, 9 standalone worksheets, and the free checklist

- Relevant Date Establishment Method — the structured approach to pinning down and documenting when cohabitation ceased. Because a one-month difference in your relevant date can swing pension values by thousands of pounds — and disagreements here are the most common cause of contested financial proceedings in Scotland.

- The Matrimonial Property Classification System — exactly how to identify what falls inside the shareable pool and what stays excluded. Covers the critical exceptions: the family home acquired before marriage for use as the matrimonial home, inheritances that have been ring-fenced versus those that have been commingled, and gifts from third parties.

- The Family Home Decision Framework — sell, buyout, or defer? Calculates net equity after mortgage, liens, and transaction costs. Covers LBTT (Land and Buildings Transaction Tax) on transfers, mortgage discharge requirements, re-registration with Registers of Scotland, and the occupancy rights both spouses hold under the Matrimonial Homes Act 1981 regardless of whose name is on the title.

- The Pension Apportionment Calculator — the statutory time-fraction formula (matrimonial membership months ÷ total membership months × CETV) applied step by step. Covers NHS Scotland pensions, SPPA (Scottish Public Pensions Agency) schemes, police and fire pensions, and private defined benefit and defined contribution schemes. Includes the three division options: pension sharing order, offsetting, and earmarking.

- The Debt Allocation Method — matrimonial debt identification, the joint-and-several liability trap (your separation agreement does not bind your creditors), credit card strategy, and the critical distinction between what a Minute of Agreement says and what the bank can still enforce against you.

- Spousal Aliment & Periodical Allowance — the difference between pre-divorce aliment and post-divorce periodical allowance, the three-year cap under Section 9(1)(d), the calculation approach courts use, and the rare circumstances that justify extension. Includes a budget planner worksheet.

- Financial Disclosure Organiser — exactly which documents to gather (bank statements, pay slips, tax returns, CETV requests, Home Reports), how to organise them for exchange, and the timeline for requesting pension valuations (allow three months).

- The Minute of Agreement Drafting Guide — Heads of Terms structure, self-proving execution requirements under the Requirements of Writing Act 1995, witness requirements, and the step-by-step process for registering in the Books of Council and Session for preservation and execution.

- Tax, CGT & LBTT Chapter — the no-gain/no-loss rule for transfers between spouses in the tax year of separation, capital gains exposure on deferred sales, and LBTT implications of property transfers. Because taking £40,000 in cash and taking £40,000 in pension rights are not the same after tax.

- Business Asset Valuation — when appreciation on a pre-marital business becomes matrimonial property, sole-trader vs. limited company treatment, offsetting strategies, and the forensic valuation process.

Who this is for

The spouse quietly gathering records before raising the topic. The person staring at a separation and realising that simplified divorce requires all finances to be settled first. The public sector worker wondering how much of a 25-year NHS pension is matrimonial property. The couple who agree on most things and want to reach a Minute of Agreement at the kitchen table without paying £1,500 for an undefended ordinary divorce — but need the calculations to prove the split is actually fair. The homemaker calculating whether they can afford to keep the house after a sole-name remortgage. And the person with a solicitor, who wants to stop paying £300 per hour for document organisation they can handle themselves.

Why not just use the free resources?

Because the free resources give you procedures, not calculations. Mygov.scot explains that you can apply for divorce and that financial matters should be resolved first. Citizens Advice Scotland outlines your general rights. Neither one tells you how to calculate the matrimonial portion of a defined benefit pension, work out a home equity buyout after LBTT and mortgage discharge costs, or figure out whether keeping the house or taking a pension offset gives you a better financial position.

The commercial alternatives — Quickie Divorce at £199–£299 — automate the court filing forms for England and Wales with limited Scottish adaptation. They don't cover the relevant date rule, the Section 9 principles, the pension apportionment formula, or the Minute of Agreement registration process. And generic UK document templates from LawDepot don't include the self-proving execution clauses or Books of Council and Session registration language that makes a Scottish agreement enforceable.

An honest guarantee

Work through the Fair Sharing Navigation System. If the guide doesn't make your financial split clearer and better organised than any blank form or free article could — email us within 30 days for a full refund. The risk of trying it is a fraction of one solicitor consultation. The risk of rushing into a simplified divorce without resolving finances is permanent: once the Extract Decree is issued, your financial claims are closed forever.

For — less than fifteen minutes of solicitor time — you get the classification system, the pension apportionment math, the worksheets, and the step-by-step sequence that the free forms leave out.

Stop staring at a warning on Form A. Get the guide, build your inventory, and walk into your separation with the numbers already done.